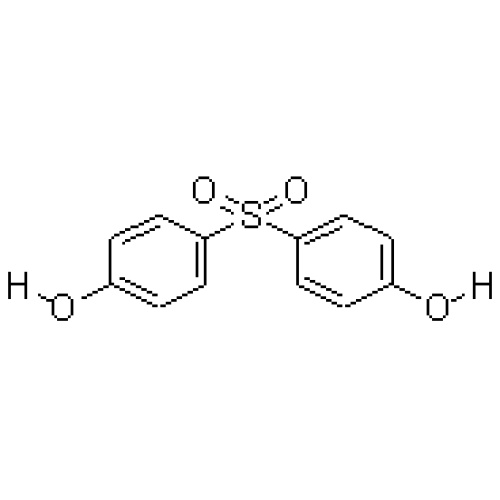

On August 29, the Ministry of Commerce issued an announcement deciding to carry out an end-of-term review of the anti-dumping measures applicable to imported bisphenol A originating in Japan, Singapore, South Korea, and China's Taiwan starting on August 30, 2012. The final review of the products under investigation is consistent with the original anti-dumping investigation and the investigation will be completed before August 30, 2013. Each node of anti-dumping cases is usually concerned by the industry, causing market fluctuations, but the market participants have said that this news has little effect on the domestic BPA market.

From the perspective of supply and demand, the current annual domestic production capacity of bisphenol A is about 600,000 tons. Most of them have matching supply directions, and there is not much outside supply. These bisphenol A products are mostly made from polycarbonate. Bayer MaterialScience (China) Co., Ltd. has an annual output of 210,000 tons of bisphenol A plant with stable start-up, and most of its products are for its polycarbonate plant; Sinopec Mitsubishi Chemical Polycarbonate (Beijing) Co., Ltd. has an annual output of 150,000 tons of bisphenol A plant Shortly after being put into operation, the products not only supply its annual production capacity of 60,000 tons of polycarbonate units, but also some external supply; Shanghai Sinopec Mitsui Chemicals Co., Ltd.'s products mainly supply Jiaxing Teijin Polycarbonate installations, some of which are external supply.

Two other domestic manufacturers of bisphenol A supply their own epoxy resin devices. Nantong Xingchen Synthetic Material Co., Ltd. Annually produces 90,000 tons of bisphenol A devices and half of its epoxy resin devices. Huizhou Zhongxin Chemical Co., Ltd. has an annual output of 25,000 tons of bisphenol A device products and an annual output of 50,000 tons of epoxy. Resin device.

Therefore, the quantity of BPA available for the domestic market is still insufficient. Domestic three-component bisphenol A is used for polycarbonate and 70% for epoxy resin. At present, the annual production capacity of polycarbonate in China is 360,000 tons. Since most of them are self-supporting, and there are few manufacturers and production concentration, they have established a stable supply chain relationship with bisphenol A; the annual production capacity of epoxy resin is 1 million tons, and most of them have no self. Supporting, and manufacturers, production and dispersion, so most of the purchase of raw materials through traders. Most of the suppliers of goods are imported. Last year, China imported 520,000 tons of bisphenol A, an increase of 32.85% over the previous year. In the first seven months of this year, it imported 300,000 tons, an increase of 2.01% over the same period last year. From the above data, it can be seen that domestic dependence on bisphenol A imports is relatively high and there is a rigid demand, and imports continued to increase during the implementation of anti-dumping measures. Therefore, the news of the review and filing of the anti-dumping case did not cause market stress.

Judging from the trend of the domestic market, the price of bisphenol A in East China has been between 12,000 and 14,000 yuan (t price, the same below). From January to April, the trend of crude oil and upstream raw materials was firm, laying the foundation for the high cost of BPA. The market's focus of discussion increased from 12,400 yuan to 14,000 yuan. However, the outlook was not long. With the downstream demand still not improving, the related product epichlorohydrin market also fell sharply. The market of bisphenol A turned to an overcast again and fell to around 13,000 yuan.

From May to June, the market of bisphenol A consolidates overcast. Downstream demand has shrunk significantly, and parking production has been a common occurrence; upstream fenone prices have accelerated, with phenols falling by as much as 16% a month. At the same time, bisphenol A plants frequently face shipping pressure and continue to cut prices to lighten up their positions. Due to the unsatisfied demand, the downstream reduced the purchase quantity and frequency again, and the price dropped to 12,000 yuan. From July to August, the prices of bisphenol A in the market fluctuate. Direct raw phenol, ** rose more than 15%, bisphenol A prices rose to close to 13,500 yuan, or about 8.5%.

Looking at the evolution of the market this year, because demand has always been weak, the market price is basically about raw material costs. In the case of sluggish demand, the degree of market attention is not high enough, and the contradiction is more focused on changes in demand and the rise and fall of raw materials. Therefore, the sensitivity of the market to the review and filing of anti-dumping investigations is quite limited.

Judging from the current market trend, under the background of weak demand pull, there will be no collapse of bisphenol A, and most manufacturers can still maintain no losses, basically benefiting from the strong phenol as the main raw material. The market price of bisphenol A surged last week and was closely related to the warming up of the market caused by the centralized overhaul of upstream phenones.

On the other hand, the price of the bisphenol A external disk was firm for 5 consecutive weeks, and the phenol and quinazones remained at a 6-week high and the cost of the external disk of bisphenol A was still at a standstill. Downstream epoxy resin manufacturers continued low stocks of raw materials, digested through the stage of inventory, the recent increase in demand for replenishment, but also to a certain extent on the market to form a support for small upswing.

Two trading days after the announcement of the Ministry of Commerce, the main importers of bisphenol A are still intent on the cost support and the production companies are also striving to stabilize prices. The final review of the anti-dumping of bisphenol A will have no material impact on the buyer and seller. The production and sales of downstream epoxy resin are generally in the market, or form the biggest limitation on the trend of bisphenol A.

Jiangxi Hongjiu New Material Technology Co.,Ltd.

Jiangxi Hongjiu New Material Technology Co.,Ltd.